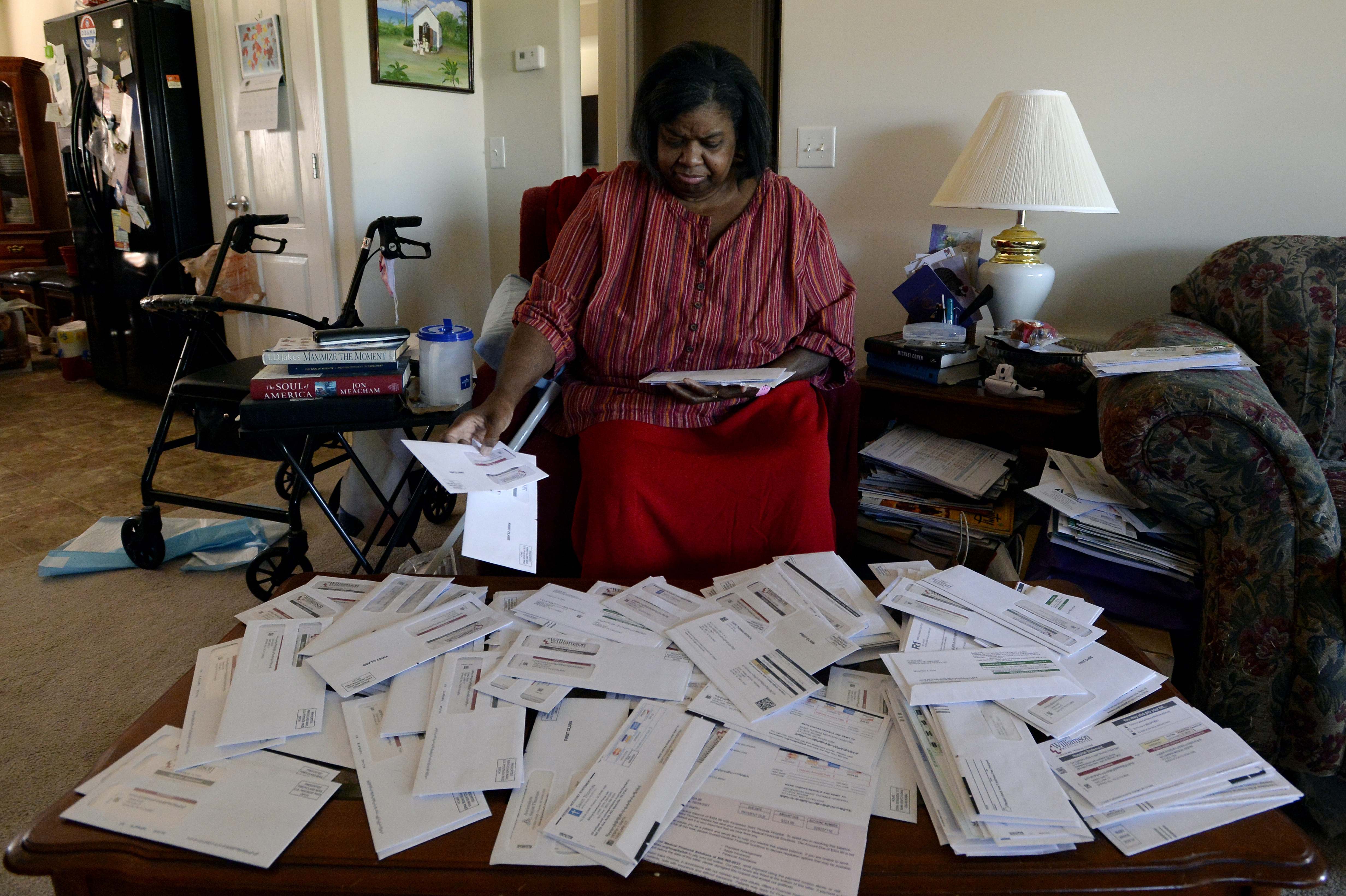

Kimberly Palmer: How to handle your medical bills

When she was 19, writer Emily Maloney found herself facing about $50,000 in medical debt after hospital treatment for a mental health crisis. The debt followed her throughout her twenties, hurting her credit and leading to stressful calls from collection agencies.

Share: